Auto insurance is required by law in nearly every US state, yet many American drivers don’t fully understand what their policy actually covers. Knowing exactly what each type of auto insurance coverage does — and doesn’t — cover can prevent expensive surprises when you need to file a claim.

This guide breaks down every major type of auto insurance coverage available to American drivers, explains when each applies, and helps you determine what combination is right for your situation.

Why Auto Insurance Coverage Matters

Auto accidents are one of the most common causes of financial hardship for American families. The average cost of a car accident resulting in injury exceeds $50,000 in medical bills, lost wages, and property damage. Without adequate insurance, these costs can fall directly on you — regardless of who was at fault.

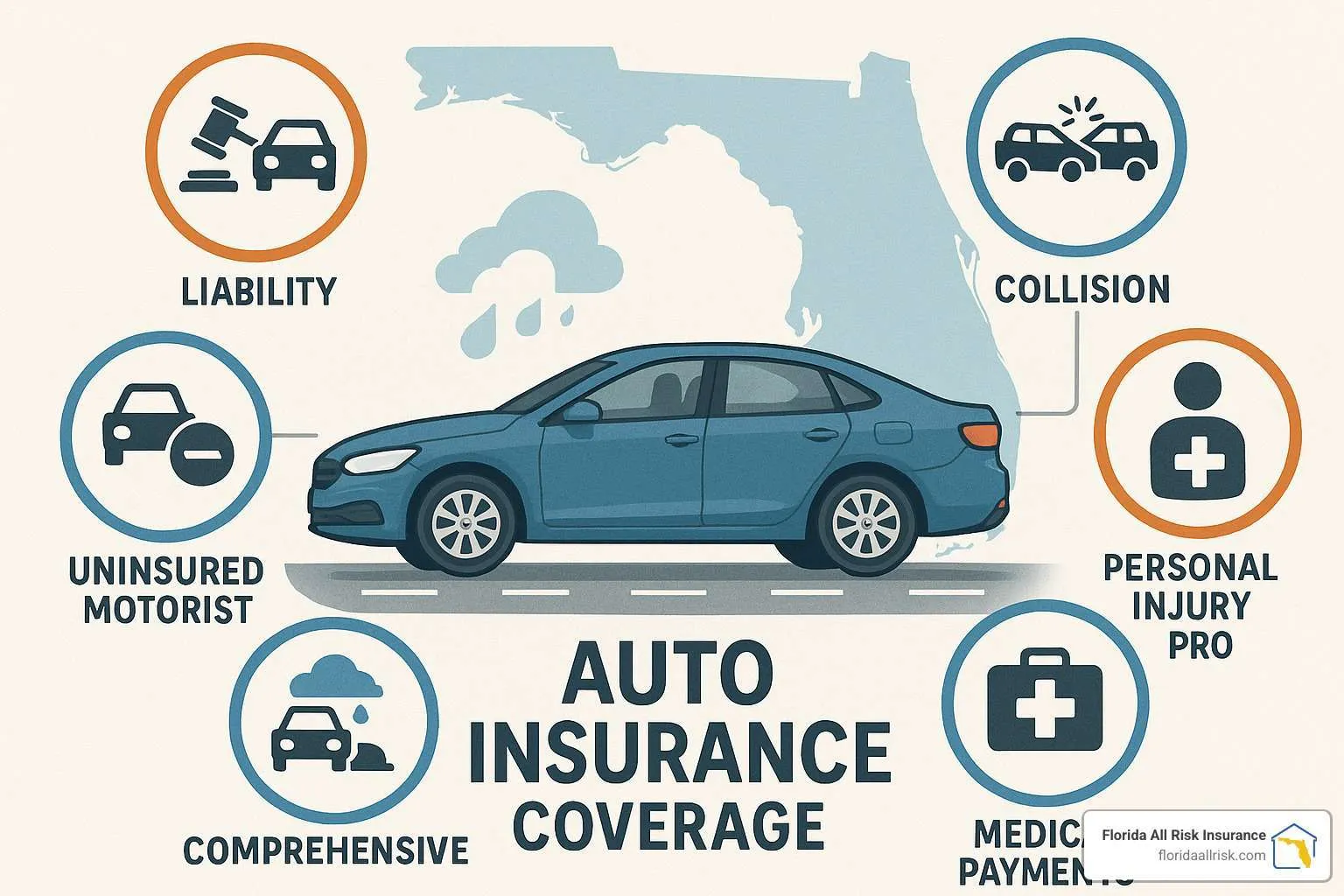

Liability Coverage: The Foundation

Bodily Injury Liability

Bodily injury liability pays for medical expenses, lost wages, and legal fees for other people injured in an accident you cause. It is required in almost every US state. Coverage is expressed as two numbers — for example, 100/300 means $100,000 per person and $300,000 per accident.

State minimum requirements are often dangerously low. A single serious accident can easily exceed $100,000 in medical costs. Most insurance professionals recommend carrying at least 100/300 in bodily injury liability.

Property Damage Liability

Covers damage you cause to other people’s vehicles or property in an accident. Also required in nearly all states. Minimum requirements are typically $10,000–$25,000, but given the cost of modern vehicles, coverage of $100,000 is advisable.

Coverage for Your Own Vehicle

Collision Coverage

Pays for damage to your own vehicle resulting from a collision with another vehicle or object, regardless of fault. If you hit a guardrail, rear-end another car, or are hit by an uninsured driver, collision coverage repairs or replaces your vehicle minus your deductible.

Collision coverage is typically required by lenders if you have a car loan or lease. For older vehicles with low market value, dropping collision coverage can save money.

Comprehensive Coverage

Covers damage to your vehicle from non-collision events including theft, vandalism, fire, flooding, hail, falling objects, and animal collisions. Despite the name, comprehensive does not cover collision damage — you need both coverages for full protection.

Protection Against Other Drivers

Uninsured Motorist Coverage (UM)

Approximately 12% of US drivers are uninsured. Uninsured motorist coverage protects you if you’re hit by a driver with no insurance, covering your medical expenses and in some states, vehicle damage. This coverage is required in about half of US states.

Underinsured Motorist Coverage (UIM)

Provides protection when the at-fault driver has insurance but their coverage limits are insufficient to cover your damages. UIM pays the difference between their coverage and your actual losses up to your policy limit.

Medical Coverages

Medical Payments Coverage (MedPay)

Pays medical expenses for you and your passengers after an accident, regardless of fault. Covers hospital bills, surgery, X-rays, and ambulance fees. Available in most states and is a relatively inexpensive add-on.

Personal Injury Protection (PIP)

Required in no-fault states, PIP provides broader coverage than MedPay. In addition to medical expenses, PIP covers lost wages, rehabilitation costs, and in some states, funeral expenses and survivor benefits. Coverage limits and required benefits vary significantly by state.

Optional Add-On Coverages

Roadside Assistance

Covers towing, battery jump-starts, flat tire changes, lockout service, and fuel delivery. Often available as an inexpensive add-on or through separate memberships like AAA.

Rental Reimbursement

Pays for a rental car while your vehicle is being repaired after a covered claim. Typically costs just a few dollars per month to add.

Gap Insurance

If you total a vehicle that you owe more on than it’s worth, gap insurance covers the difference between your vehicle’s actual cash value and your remaining loan balance. Essential for new vehicle purchases and leases.

Recommended Coverage Levels

| Coverage Type | Recommended Minimum |

| Bodily Injury Liability | $100,000/$300,000 |

| Property Damage Liability | $100,000 |

| Uninsured Motorist | Match liability limits |

| Collision Deductible | $500 – $1,000 |

| Comprehensive Deductible | $250 – $500 |

Final Thoughts

Understanding your auto insurance coverage is one of the most practical financial literacy skills an American driver can develop. Review your policy documents, make sure your coverage limits reflect your actual financial exposure, and shop for quotes annually to ensure you’re getting the best value for your premium dollar.